Restez informé

Restez informé. Consultez les publications qui peuvent vous être utiles ou vérifiez si un événement a lieu dans votre secteur. Revenez régulièrement; cette page est tenue à jour et contient beaucoup de renseignements pertinents.

Did you know that payout annuities can help provide financial predictability in retirement?

Benefits include:

• Reliable monthly income

• Protection against market volatility

• No investment management required

• Peace of mind planning

Discover how guaranteed income streams can complement retirement portfolios and provide stability. Let’s chat! https://advisor.sunlife.ca/donatina.monaco/

Benefits include:

• Reliable monthly income

• Protection against market volatility

• No investment management required

• Peace of mind planning

Discover how guaranteed income streams can complement retirement portfolios and provide stability. Let’s chat! https://advisor.sunlife.ca/donatina.monaco/

Did you know that payout annuities can help provide financial predictability in retirement?

Benefits include:

• Reliable monthly income

• Protection against market volatility

• No investment management required

• Peace of mind planning

Discover how guaranteed income streams can complement retirement portfolios and provide stability. Let’s chat! https://advisor.sunlife.ca/donatina.monaco/

Benefits include:

• Reliable monthly income

• Protection against market volatility

• No investment management required

• Peace of mind planning

Discover how guaranteed income streams can complement retirement portfolios and provide stability. Let’s chat! https://advisor.sunlife.ca/donatina.monaco/

Saviez-vous que vous pouvez encore cotiser à votre REER pour 2025? Vous avez jusqu’au 2 mars 2026. Communiquez avec moi pour savoir s’il s’agit d’une bonne option pour vous!

Saviez-vous que vous pouvez encore cotiser à votre REER pour 2025? Vous avez jusqu’au 2 mars 2026. Communiquez avec moi pour savoir s’il s’agit d’une bonne option pour vous!

Did you know you can still contribute to your 2025 RRSP before March 2, 2026? Get in touch with me to find out if that’s a good idea for you!

Did you know you can still contribute to your 2025 RRSP before March 2, 2026? Get in touch with me to find out if that’s a good idea for you!

Do you want to keep more money in your business? Let's talk about smart tax strategies that fit your company to make it more tax efficient. 📊

Ready to save? Visit my website to set up time to chat. https://advisor.sunlife.ca/donatina.monaco/

Ready to save? Visit my website to set up time to chat. https://advisor.sunlife.ca/donatina.monaco/

Do you want to keep more money in your business? Let's talk about smart tax strategies that fit your company to make it more tax efficient. 📊

Ready to save? Visit my website to set up time to chat. https://advisor.sunlife.ca/donatina.monaco/

Ready to save? Visit my website to set up time to chat. https://advisor.sunlife.ca/donatina.monaco/

Feeling the winter blahs? You're not alone. There’s still time to prioritize your mental wellbeing this winter. Many Sun Life plans offer coverage for mental health services. Let's discuss how your insurance can support you.

Feeling the winter blahs? You're not alone. There’s still time to prioritize your mental wellbeing this winter. Many Sun Life plans offer coverage for mental health services. Let's discuss how your insurance can support you.

Navigating life insurance options can be overwhelming. Whether finishing school, buying a first home or starting a family, finding the right plan that fits life's unique journey is essential.

We can help secure your future together. Let us know how we can help.

We can help secure your future together. Let us know how we can help.

Navigating life insurance options can be overwhelming. Whether finishing school, buying a first home or starting a family, finding the right plan that fits life's unique journey is essential.

We can help secure your future together. Let us know how we can help.

We can help secure your future together. Let us know how we can help.

Family is everything! When you meet with me, we’ll discuss how you can plan to protect them no matter what life throws at you, the expected and the unexpected.

Family is everything! When you meet with me, we’ll discuss how you can plan to protect them no matter what life throws at you, the expected and the unexpected.

La famille, ça vaut de l’or! Prenons un moment pour discuter des plans que vous pouvez mettre en place pour la protéger des imprévus, quoi que la vie vous réserve.

La famille, ça vaut de l’or! Prenons un moment pour discuter des plans que vous pouvez mettre en place pour la protéger des imprévus, quoi que la vie vous réserve.

Thoughtful planning ensures your assets reach the right people at the right time — with minimal tax impact.

Key considerations include:

-Estate planning strategies

-Tax-efficient wealth transfer

-Protecting family harmony

-Preserving your legacy

Start planning today for a seamless transition tomorrow. Get in touch today. https://advisor.sunlife.ca/donatina.monaco/

Key considerations include:

-Estate planning strategies

-Tax-efficient wealth transfer

-Protecting family harmony

-Preserving your legacy

Start planning today for a seamless transition tomorrow. Get in touch today. https://advisor.sunlife.ca/donatina.monaco/

Thoughtful planning ensures your assets reach the right people at the right time — with minimal tax impact.

Key considerations include:

-Estate planning strategies

-Tax-efficient wealth transfer

-Protecting family harmony

-Preserving your legacy

Start planning today for a seamless transition tomorrow. Get in touch today. https://advisor.sunlife.ca/donatina.monaco/

Key considerations include:

-Estate planning strategies

-Tax-efficient wealth transfer

-Protecting family harmony

-Preserving your legacy

Start planning today for a seamless transition tomorrow. Get in touch today. https://advisor.sunlife.ca/donatina.monaco/

Building wealth is about more than growing your money – it's about creating lasting financial security. 💖💰

Your financial wellbeing matters at every stage of life. Whether you're just starting out or well into your journey, now is the right time to take action.

Ready to connect? Let's work together to help you set achievable long-term wealth goals and build a brighter financial future.

Your financial wellbeing matters at every stage of life. Whether you're just starting out or well into your journey, now is the right time to take action.

Ready to connect? Let's work together to help you set achievable long-term wealth goals and build a brighter financial future.

Building wealth is about more than growing your money – it's about creating lasting financial security. 💖💰

Your financial wellbeing matters at every stage of life. Whether you're just starting out or well into your journey, now is the right time to take action.

Ready to connect? Let's work together to help you set achievable long-term wealth goals and build a brighter financial future.

Your financial wellbeing matters at every stage of life. Whether you're just starting out or well into your journey, now is the right time to take action.

Ready to connect? Let's work together to help you set achievable long-term wealth goals and build a brighter financial future.

Strategic planning can help you make the most of housing transitions.

Have you considered:

-Capital gains implications?

-Mortgage protection during transition?

-Investment of home equity?

-Lifestyle considerations?

Professional advice ensures housing decisions align with your overall retirement goals. Let's discuss the financial aspects of downsizing.

#RetirementPlanning #Retirement

Have you considered:

-Capital gains implications?

-Mortgage protection during transition?

-Investment of home equity?

-Lifestyle considerations?

Professional advice ensures housing decisions align with your overall retirement goals. Let's discuss the financial aspects of downsizing.

#RetirementPlanning #Retirement

Strategic planning can help you make the most of housing transitions.

Have you considered:

-Capital gains implications?

-Mortgage protection during transition?

-Investment of home equity?

-Lifestyle considerations?

Professional advice ensures housing decisions align with your overall retirement goals. Let's discuss the financial aspects of downsizing.

#RetirementPlanning #Retirement

Have you considered:

-Capital gains implications?

-Mortgage protection during transition?

-Investment of home equity?

-Lifestyle considerations?

Professional advice ensures housing decisions align with your overall retirement goals. Let's discuss the financial aspects of downsizing.

#RetirementPlanning #Retirement

Business owners, are you so focused on your company that your personal finances have been put on hold?

Let's work together to create a financial roadmap that supports both your business ambitions and personal dreams.

Get started here > https://advisor.sunlife.ca/donatina.monaco/

Let's work together to create a financial roadmap that supports both your business ambitions and personal dreams.

Get started here > https://advisor.sunlife.ca/donatina.monaco/

Business owners, are you so focused on your company that your personal finances have been put on hold?

Let's work together to create a financial roadmap that supports both your business ambitions and personal dreams.

Get started here > https://advisor.sunlife.ca/donatina.monaco/

Let's work together to create a financial roadmap that supports both your business ambitions and personal dreams.

Get started here > https://advisor.sunlife.ca/donatina.monaco/

Épargnez-vous assez dans votre REER pour vivre la retraite rêvée? Entrez vos chiffres dans le calculateur gratuit de la Sun Life. Prenons ensuite contact pour discuter de vos options.

Épargnez-vous assez dans votre REER pour vivre la retraite rêvée? Entrez vos chiffres dans le calculateur gratuit de la Sun Life. Prenons ensuite contact pour discuter de vos options.

Are you saving enough in your RRSP for the retirement you want? Crunch the numbers in Sun Life's free RRSP calculator. Then, let’s connect and talk about your options.

https://www.sunlife.ca/en/tools-and-resources/tools-and-calculators/rrsp-calculator/

https://www.sunlife.ca/en/tools-and-resources/tools-and-calculators/rrsp-calculator/

Are you saving enough in your RRSP for the retirement you want? Crunch the numbers in Sun Life's free RRSP calculator. Then, let’s connect and talk about your options.

https://www.sunlife.ca/en/tools-and-resources/tools-and-calculators/rrsp-calculator/

https://www.sunlife.ca/en/tools-and-resources/tools-and-calculators/rrsp-calculator/

Avez-vous mis toute votre attention sur votre entreprise que vous en avez négligé vos finances personnelles? Le moment est venu d’adopter une approche globale.

Travaillons ensemble pour créer un parcours financier qui cadre avec vos ambitions professionnelles et vos rêves personnels.

Ça commence ici > https://advisor.sunlife.ca/donatina.monaco/

Travaillons ensemble pour créer un parcours financier qui cadre avec vos ambitions professionnelles et vos rêves personnels.

Ça commence ici > https://advisor.sunlife.ca/donatina.monaco/

Avez-vous mis toute votre attention sur votre entreprise que vous en avez négligé vos finances personnelles? Le moment est venu d’adopter une approche globale.

Travaillons ensemble pour créer un parcours financier qui cadre avec vos ambitions professionnelles et vos rêves personnels.

Ça commence ici > https://advisor.sunlife.ca/donatina.monaco/

Travaillons ensemble pour créer un parcours financier qui cadre avec vos ambitions professionnelles et vos rêves personnels.

Ça commence ici > https://advisor.sunlife.ca/donatina.monaco/

February is Heart Health Month. Heart disease affects 1 in 12 Canadian adults – a reminder of why protecting both your health and your financial wellbeing matters.

Critical illness insurance can help provide financial support when you need it most, helping you focus on recovery without the added stress of financial uncertainty. Find out more. Let's connect!

Critical illness insurance can help provide financial support when you need it most, helping you focus on recovery without the added stress of financial uncertainty. Find out more. Let's connect!

February is Heart Health Month. Heart disease affects 1 in 12 Canadian adults – a reminder of why protecting both your health and your financial wellbeing matters.

Critical illness insurance can help provide financial support when you need it most, helping you focus on recovery without the added stress of financial uncertainty. Find out more. Let's connect!

Critical illness insurance can help provide financial support when you need it most, helping you focus on recovery without the added stress of financial uncertainty. Find out more. Let's connect!

Time flies by, and tuition costs fly sky-high. 🕰️💸 When it comes to education costs for your kid(s), it pays to start early and save consistently. Small RESP contributions can add up over time.

Want to explore how to optimize saving for your child(ren)’s education? Let's chat about creating a plan that fits your family's budget. https://advisor.sunlife.ca/donatina.monaco/

Want to explore how to optimize saving for your child(ren)’s education? Let's chat about creating a plan that fits your family's budget. https://advisor.sunlife.ca/donatina.monaco/

Time flies by, and tuition costs fly sky-high. 🕰️💸 When it comes to education costs for your kid(s), it pays to start early and save consistently. Small RESP contributions can add up over time.

Want to explore how to optimize saving for your child(ren)’s education? Let's chat about creating a plan that fits your family's budget. https://advisor.sunlife.ca/donatina.monaco/

Want to explore how to optimize saving for your child(ren)’s education? Let's chat about creating a plan that fits your family's budget. https://advisor.sunlife.ca/donatina.monaco/

Life changes, goals evolve and your estate plan should too.

Whether navigating business succession, protecting family wealth or maximizing tax efficiency, we can help ensure your legacy reflects your current vision and helps protect what matters most.

Ready to review your plan? Reach out today. https://advisor.sunlife.ca/donatina.monaco/

Whether navigating business succession, protecting family wealth or maximizing tax efficiency, we can help ensure your legacy reflects your current vision and helps protect what matters most.

Ready to review your plan? Reach out today. https://advisor.sunlife.ca/donatina.monaco/

Life changes, goals evolve and your estate plan should too.

Whether navigating business succession, protecting family wealth or maximizing tax efficiency, we can help ensure your legacy reflects your current vision and helps protect what matters most.

Ready to review your plan? Reach out today. https://advisor.sunlife.ca/donatina.monaco/

Whether navigating business succession, protecting family wealth or maximizing tax efficiency, we can help ensure your legacy reflects your current vision and helps protect what matters most.

Ready to review your plan? Reach out today. https://advisor.sunlife.ca/donatina.monaco/

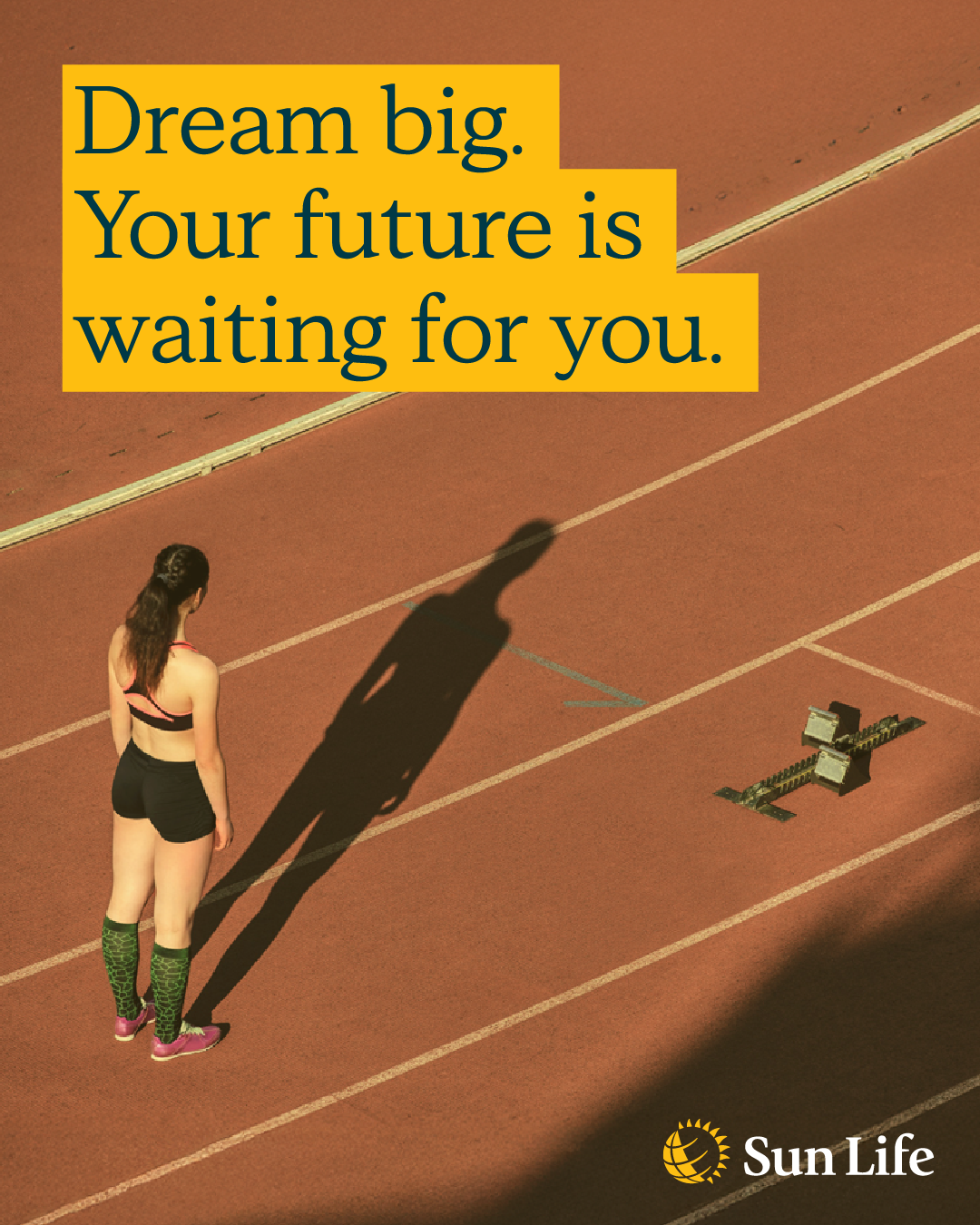

Dreaming big for your future? Let's talk about how we help turn those dreams into reality. Whether it's early retirement or a new business venture, let's create a strategy to get you there.

Reach out to start your journey!

Reach out to start your journey!

Dreaming big for your future? Let's talk about how we help turn those dreams into reality. Whether it's early retirement or a new business venture, let's create a strategy to get you there.

Reach out to start your journey!

Reach out to start your journey!

Financial advice that fits your needs. Let Sun Life One Plan help.

Create your personalized roadmap with Sun Life One Plan! This powerful tool helps you set achievable goals and brings your financial dreams closer to reality. https://sunlife.hubs.vidyard.com/watch/ksLWJjT43furjobhkXkgiQ

Take control of your financial future. Reach out today to get started!

#RetirementPlanning #SunLifeOnePlan

Take control of your financial future. Reach out today to get started!

#RetirementPlanning #SunLifeOnePlan

Voir la vidéo

Des questions?

Ici pour répondre à vos questions, expliquer les produits et vous aider à faire les premiers pas pour atteindre vos objectifs.

Nous sommes liés par contrat à Distribution Financière Sun Life (Canada) inc., une compagnie d'assurance-vie, membre du groupe Financière Sun Life. Fonds communs de placement offerts par Placements Financière Sun Life (Canada) inc.