Restez informé

Restez informé. Consultez les publications qui peuvent vous être utiles ou vérifiez si un événement a lieu dans votre secteur. Revenez régulièrement; cette page est tenue à jour et contient beaucoup de renseignements pertinents.

La vie est imprévisible. Une protection appropriée peut vous aider à préserver votre sécurité financière dans les moments les plus importants. L’assurance peut jouer un rôle clé dans votre approche financière globale. Passons en revue votre couverture et assurons-nous qu’elle correspond à vos besoins. https://conseiller.sunlife.ca/f/meyer.elbaz

La vie est imprévisible. Une protection appropriée peut vous aider à préserver votre sécurité financière dans les moments les plus importants. L’assurance peut jouer un rôle clé dans votre approche financière globale. Passons en revue votre couverture et assurons-nous qu’elle correspond à vos besoins. https://conseiller.sunlife.ca/f/meyer.elbaz

Buying a home, growing your family, building your career — there’s a lot to balance. Creating a personalized financial roadmap early can help you stay on track while still living for today. Small steps today can make a meaningful difference over time. Get in touch to discuss options that will work best for you. https://advisor.sunlife.ca/meyer.elbaz

Buying a home, growing your family, building your career — there’s a lot to balance. Creating a personalized financial roadmap early can help you stay on track while still living for today. Small steps today can make a meaningful difference over time. Get in touch to discuss options that will work best for you. https://advisor.sunlife.ca/meyer.elbaz

Acheter une maison, agrandir votre famille, faire progresser votre carrière : tout cela demande de l’équilibre. Élaborons un parcours financier personnalisé dès maintenant pour vous aider à rester sur la bonne voie tout en profitant du moment présent. Les petits gestes d’aujourd’hui peuvent faire toute la différence à long terme. https://conseiller.sunlife.ca/f/meyer.elbaz

Acheter une maison, agrandir votre famille, faire progresser votre carrière : tout cela demande de l’équilibre. Élaborons un parcours financier personnalisé dès maintenant pour vous aider à rester sur la bonne voie tout en profitant du moment présent. Les petits gestes d’aujourd’hui peuvent faire toute la différence à long terme. https://conseiller.sunlife.ca/f/meyer.elbaz

You’ve built significant wealth. Now it’s about making it last. With the right approach, you can help reduce tax impacts, protect your estate and create a legacy that supports the people and causes you care about. Let’s build a strategy that helps you move into retirement with clarity and confidence. Book a conversation to start shaping your legacy. https://advisor.sunlife.ca/meyer.elbaz

You’ve built significant wealth. Now it’s about making it last. With the right approach, you can help reduce tax impacts, protect your estate and create a legacy that supports the people and causes you care about. Let’s build a strategy that helps you move into retirement with clarity and confidence. Book a conversation to start shaping your legacy. https://advisor.sunlife.ca/meyer.elbaz

Vous avez constitué un patrimoine important. Le moment est venu de le pérenniser. Avec la bonne approche, vous pouvez réduire les répercussions fiscales, protéger votre succession et créer un héritage qui soutient les personnes et les causes qui vous sont chères. Élaborons ensemble une stratégie claire qui vous permettra de prendre votre retraite en toute quiétude. Prenez rendez-vous pour commencer à façonner votre héritage. https://conseiller.sunlife.ca/f/meyer.elbaz

Vous avez constitué un patrimoine important. Le moment est venu de le pérenniser. Avec la bonne approche, vous pouvez réduire les répercussions fiscales, protéger votre succession et créer un héritage qui soutient les personnes et les causes qui vous sont chères. Élaborons ensemble une stratégie claire qui vous permettra de prendre votre retraite en toute quiétude. Prenez rendez-vous pour commencer à façonner votre héritage. https://conseiller.sunlife.ca/f/meyer.elbaz

Life can be unpredictable. The right protection can help you stay financially secure when it matters most. Insurance can play a key role in supporting your overall financial approach. Let’s review your coverage and make sure it fits your needs. https://advisor.sunlife.ca/meyer.elbaz

Life can be unpredictable. The right protection can help you stay financially secure when it matters most. Insurance can play a key role in supporting your overall financial approach. Let’s review your coverage and make sure it fits your needs. https://advisor.sunlife.ca/meyer.elbaz

Avec un parcours financier bien structuré, vous vous assurez que votre patrimoine soutiendra les personnes et les causes qui vous tiennent à cœur, d’une génération à l’autre.

Ensemble, façonnons un héritage qui reflète votre vision grâce à Un Plan, simplement Sun Life. Communiquez avec nous pour commencer. https://conseiller.sunlife.ca/f/meyer.elbaz

#UnPlanSimplementSunLife #SunLife

Ensemble, façonnons un héritage qui reflète votre vision grâce à Un Plan, simplement Sun Life. Communiquez avec nous pour commencer. https://conseiller.sunlife.ca/f/meyer.elbaz

#UnPlanSimplementSunLife #SunLife

Avec un parcours financier bien structuré, vous vous assurez que votre patrimoine soutiendra les personnes et les causes qui vous tiennent à cœur, d’une génération à l’autre.

Ensemble, façonnons un héritage qui reflète votre vision grâce à Un Plan, simplement Sun Life. Communiquez avec nous pour commencer. https://conseiller.sunlife.ca/f/meyer.elbaz

#UnPlanSimplementSunLife #SunLife

Ensemble, façonnons un héritage qui reflète votre vision grâce à Un Plan, simplement Sun Life. Communiquez avec nous pour commencer. https://conseiller.sunlife.ca/f/meyer.elbaz

#UnPlanSimplementSunLife #SunLife

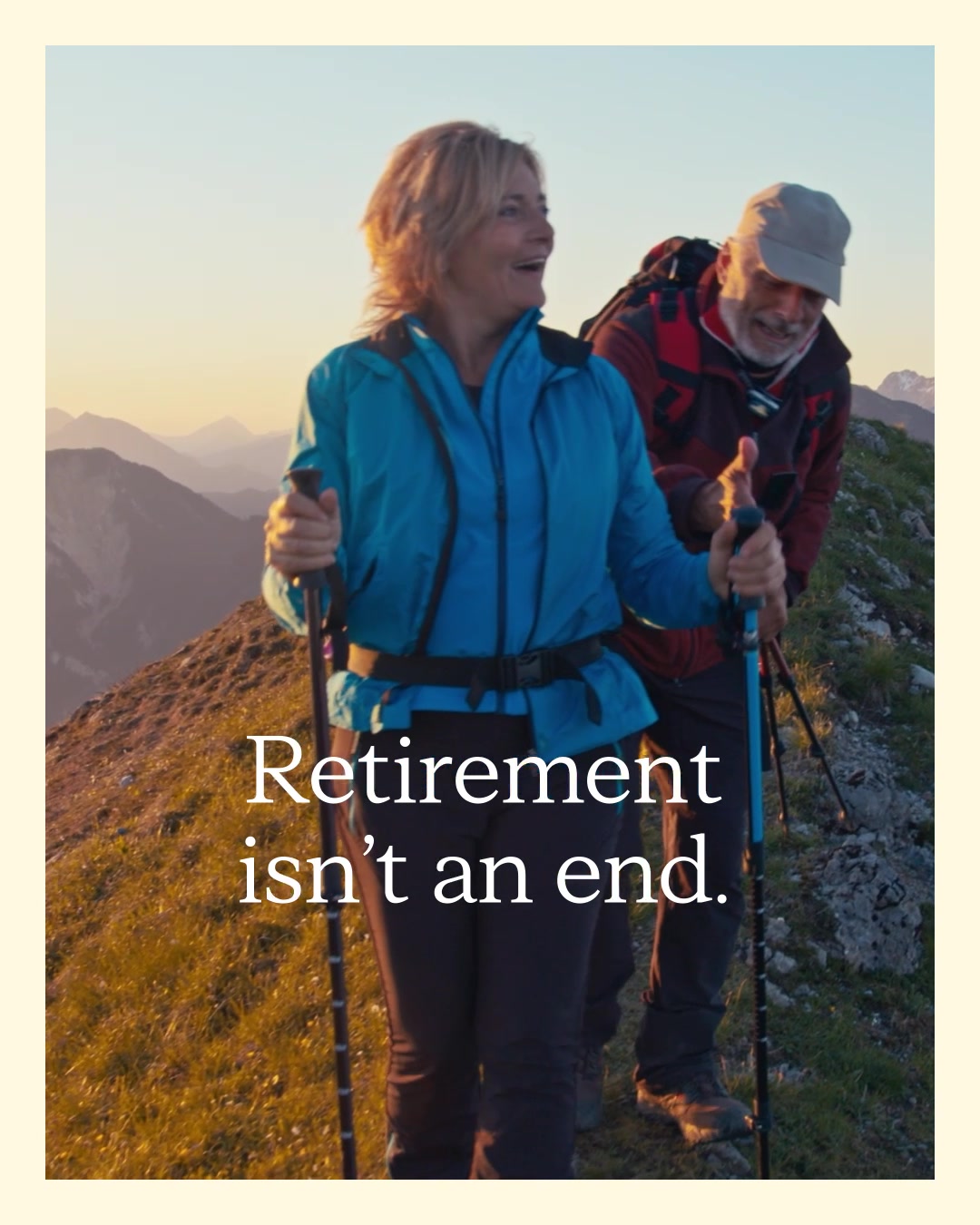

Retirement isn’t an end. It’s your next chapter.

Retirement looks different for everyone. Whether you’re planning to slow down, travel, or explore new passions, having a thoughtful strategy can help you get there with confidence. Explore ways to transition your savings into income that supports the lifestyle you envision. Let’s build a strategy that helps you move into retirement with clarity and confidence.

Voir la vidéo

L’épargne n’est qu’une partie de l’équation de la retraite. Avec une stratégie pour transformer cette épargne en revenu fiable, vous pourrez maintenir votre style de vie au fil du temps. Traçons ensemble une voie claire vers la retraite de vos rêves. https://conseiller.sunlife.ca/f/meyer.elbaz

L’épargne n’est qu’une partie de l’équation de la retraite. Avec une stratégie pour transformer cette épargne en revenu fiable, vous pourrez maintenir votre style de vie au fil du temps. Traçons ensemble une voie claire vers la retraite de vos rêves. https://conseiller.sunlife.ca/f/meyer.elbaz

Vous avez travaillé dur pour bâtir votre entreprise, mais sans étapes définies pour l’avenir, les transitions pourraient la mettre en péril.

Avec une stratégie de relève claire, vous pourrez protéger votre entreprise, soutenir votre équipe et bien tracer la voie à suivre. Prenez rendez-vous pour discuter des prochaines étapes. https://conseiller.sunlife.ca/f/meyer.elbaz

Avec une stratégie de relève claire, vous pourrez protéger votre entreprise, soutenir votre équipe et bien tracer la voie à suivre. Prenez rendez-vous pour discuter des prochaines étapes. https://conseiller.sunlife.ca/f/meyer.elbaz

Vous avez travaillé dur pour bâtir votre entreprise, mais sans étapes définies pour l’avenir, les transitions pourraient la mettre en péril.

Avec une stratégie de relève claire, vous pourrez protéger votre entreprise, soutenir votre équipe et bien tracer la voie à suivre. Prenez rendez-vous pour discuter des prochaines étapes. https://conseiller.sunlife.ca/f/meyer.elbaz

Avec une stratégie de relève claire, vous pourrez protéger votre entreprise, soutenir votre équipe et bien tracer la voie à suivre. Prenez rendez-vous pour discuter des prochaines étapes. https://conseiller.sunlife.ca/f/meyer.elbaz

You’ve worked hard to build your business, but without clear next steps, transitions could put it at risk.

A clear succession strategy can help protect your business, support your team, and create a smoother path forward. Book a quick chat to discuss your next steps. https://advisor.sunlife.ca/meyer.elbaz

A clear succession strategy can help protect your business, support your team, and create a smoother path forward. Book a quick chat to discuss your next steps. https://advisor.sunlife.ca/meyer.elbaz

You’ve worked hard to build your business, but without clear next steps, transitions could put it at risk.

A clear succession strategy can help protect your business, support your team, and create a smoother path forward. Book a quick chat to discuss your next steps. https://advisor.sunlife.ca/meyer.elbaz

A clear succession strategy can help protect your business, support your team, and create a smoother path forward. Book a quick chat to discuss your next steps. https://advisor.sunlife.ca/meyer.elbaz

Les problèmes de santé peuvent survenir sans avertissement et les coûts ne sont pas toujours d’ordre médical. L’assurance maladies graves fournit un soutien financier lors d’un diagnostic de maladie grave. Elle peut aider à couvrir les frais liés à un arrêt de travail et aux déplacements pour les soins, ou même les dépenses quotidiennes, afin que vous puissiez vous concentrer sur votre rétablissement. Voulez-vous explorer si cette assurance pour s’intégrer dans votre plan? https://conseiller.sunlife.ca/f/meyer.elbaz

Les problèmes de santé peuvent survenir sans avertissement et les coûts ne sont pas toujours d’ordre médical. L’assurance maladies graves fournit un soutien financier lors d’un diagnostic de maladie grave. Elle peut aider à couvrir les frais liés à un arrêt de travail et aux déplacements pour les soins, ou même les dépenses quotidiennes, afin que vous puissiez vous concentrer sur votre rétablissement. Voulez-vous explorer si cette assurance pour s’intégrer dans votre plan? https://conseiller.sunlife.ca/f/meyer.elbaz

Health events can happen without warning — and the costs aren’t always medical. Critical illness insurance can provide financial support during a serious diagnosis, helping with time off work, travel for care, or everyday expenses so you can focus on recovery. Want to explore if it fits your plan? https://advisor.sunlife.ca/meyer.elbaz

Health events can happen without warning — and the costs aren’t always medical. Critical illness insurance can provide financial support during a serious diagnosis, helping with time off work, travel for care, or everyday expenses so you can focus on recovery. Want to explore if it fits your plan? https://advisor.sunlife.ca/meyer.elbaz

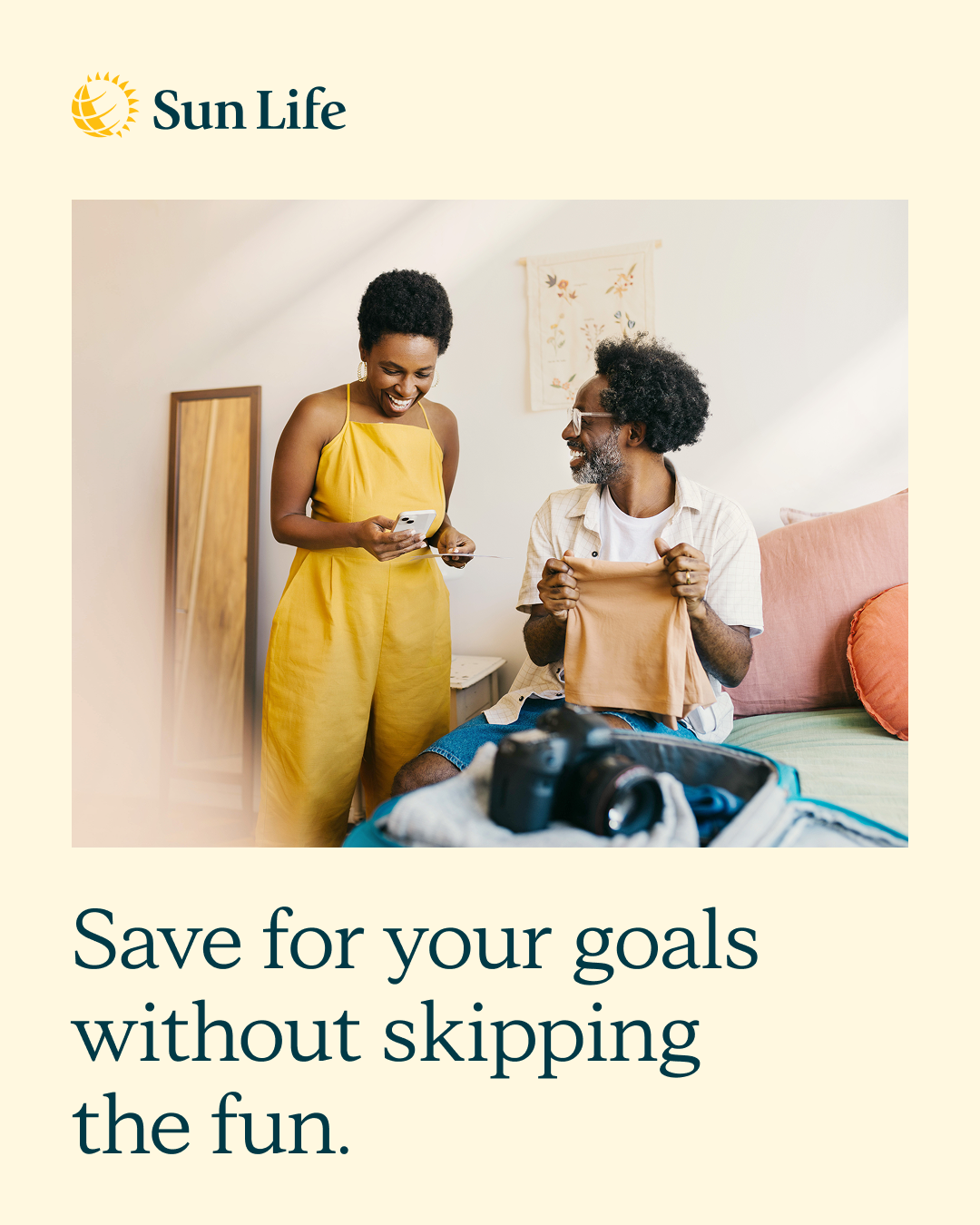

Saving for your goals shouldn’t mean skipping the fun. Whether you’re planning travel, a wedding, a big experience or your next “chapter,” the right strategy can help you set aside cash intentionally while still staying on track. Let's transform your priorities into a financial roadmap you can commit to. https://advisor.sunlife.ca/meyer.elbaz

Saving for your goals shouldn’t mean skipping the fun. Whether you’re planning travel, a wedding, a big experience or your next “chapter,” the right strategy can help you set aside cash intentionally while still staying on track. Let's transform your priorities into a financial roadmap you can commit to. https://advisor.sunlife.ca/meyer.elbaz

Épargner pour vos objectifs ne devrait pas signifier renoncer au plaisir. Que vous planifiiez un voyage, un mariage, une grande expérience ou votre prochain « chapitre », la bonne stratégie peut vous aider à mettre de l’argent de côté tout en restant sur la bonne voie. Transformons vos priorités en un parcours financier que vous pourrez vous engager à suivre. https://conseiller.sunlife.ca/f/meyer.elbaz

Épargner pour vos objectifs ne devrait pas signifier renoncer au plaisir. Que vous planifiiez un voyage, un mariage, une grande expérience ou votre prochain « chapitre », la bonne stratégie peut vous aider à mettre de l’argent de côté tout en restant sur la bonne voie. Transformons vos priorités en un parcours financier que vous pourrez vous engager à suivre. https://conseiller.sunlife.ca/f/meyer.elbaz

Un patrimoine important peut amener son lot de complexité. Des approches fiscalement avantageuses aux considérations successorales, un plan réfléchi vous permettra de protéger et préserver ce qui compte le plus pour vous, aujourd’hui et dans l’avenir. Simplifions les prochaines étapes en élaborant un parcours personnalisé. https://conseiller.sunlife.ca/f/meyer.elbaz

Un patrimoine important peut amener son lot de complexité. Des approches fiscalement avantageuses aux considérations successorales, un plan réfléchi vous permettra de protéger et préserver ce qui compte le plus pour vous, aujourd’hui et dans l’avenir. Simplifions les prochaines étapes en élaborant un parcours personnalisé. https://conseiller.sunlife.ca/f/meyer.elbaz

Greater wealth can bring greater complexity. From tax-aware approaches to estate considerations, having a thoughtful plan in place can help you protect and preserve what matters most — today and for the future. Let’s help simplify your next steps with a personalized roadmap. https://advisor.sunlife.ca/meyer.elbaz

Greater wealth can bring greater complexity. From tax-aware approaches to estate considerations, having a thoughtful plan in place can help you protect and preserve what matters most — today and for the future. Let’s help simplify your next steps with a personalized roadmap. https://advisor.sunlife.ca/meyer.elbaz

When your money is spread across different accounts, having one clear plan can help it work better for you over time. If you’re managing milestone goals like a home, family, retirement, or what you want to leave behind, it helps when everything connects. Let’s put a strategy together that helps support what you want next. https://advisor.sunlife.ca/meyer.elbaz

When your money is spread across different accounts, having one clear plan can help it work better for you over time. If you’re managing milestone goals like a home, family, retirement, or what you want to leave behind, it helps when everything connects. Let’s put a strategy together that helps support what you want next. https://advisor.sunlife.ca/meyer.elbaz

Lorsque votre argent est réparti dans divers comptes, avoir un plan clair peut l’aider à mieux travailler pour vous au fil du temps. Si vous avez des objectifs importants comme une maison, une famille, la retraite ou un héritage, il est préférable que ces éléments forment un tout cohérent. Établissons ensemble une stratégie qui vous aidera à obtenir ce que vous souhaitez. https://conseiller.sunlife.ca/f/meyer.elbaz

Lorsque votre argent est réparti dans divers comptes, avoir un plan clair peut l’aider à mieux travailler pour vous au fil du temps. Si vous avez des objectifs importants comme une maison, une famille, la retraite ou un héritage, il est préférable que ces éléments forment un tout cohérent. Établissons ensemble une stratégie qui vous aidera à obtenir ce que vous souhaitez. https://conseiller.sunlife.ca/f/meyer.elbaz

Ease into retirement with Sun Life One Plan

Your retirement plan should feel unique and tailored to you. Sun Life One Plan can help bring your goals, investments and income strategy together so you can see what’s possible. Get in touch to start planning your dream retirement. https://advisor.sunlife.ca/meyer.elbaz

#SunLifeOnePlan #RetirementPlanning

#SunLifeOnePlan #RetirementPlanning

Voir la vidéo

Des questions?

Ici pour répondre à vos questions, expliquer les produits et vous aider à faire les premiers pas pour atteindre vos objectifs.